The post Will Rising Costs Curb Sunbelt Growth? appeared first on Yardi Matrix Blog.

]]>Rising Expenses in Low-Cost Markets

Yet expenses, particularly insurance, recently have soared in many of these low-cost markets. Yardi Matrix found that total multifamily expenses increased 9.3% nationally year-over-year on trailing-12 basis through mid-year 2023, while markets including Tampa (16.2%), Orlando (15.1%) Austin (11.1%) and Charlotte (10.9%) saw bigger jumps. Insurance premiums rose 18.8% nationally per unit, with significantly higher increases in states with large numbers of weather-related payouts. Some of the largest property insurance increases on the metro level during that period were in Orlando (34.5%), Houston (31.6%), Tampa (28.8%), San Antonio (27.7%) and Dallas (24.3%), per Matrix.

Growth in expenses has been higher in markets where costs currently are lower. That leads to a question: will rising insurance and other expenses put a brake on development in high-growth regions?

The idea is not as far out in left field as it seems at first blush. In fact, the Dallas Federal Reserve warned in a recent publication that rising temperatures can reduce GDP growth. For every 1-degree increase in average summer temperature, Texas annual nominal GDP growth slows 0.4 percentage points, the report said. Leisure and hospitality were most impacted, but transportation, manufacturing and retail also slowed.

The Dallas Fed’s report said 2023’s heat wave reduced Texas GDP between $10 billion and $24 billion, and the problem will only intensify if projected temperatures rise in coming decades. “As climate change’s effects intensify over the next decade, heat waves will become more commonplace and severe, and Texans will need to adapt,” the report said.

Impact of Climate Change

Population and commercial property inventory are migrating most rapidly to many places where climate change is getting tangibly worse, noted Ryan Severino, chief economist at investment manager BentallGreenOak. As people and businesses continue to move to those places, coupled with climate change, environmental challenges are going to persist and likely worsen, he said. “The data is still largely anecdotal at this point because it is difficult to disentangle that specific effect from the broader slowdown after the pandemic boom,” Severino said. “But at the margin it is starting to have an impact on demographic changes.”

The most obvious hurdle for commercial properties is rising insurance premiums due to the growing number of weather-related payouts. Not only are premiums increasing, but policies offer less coverage with higher deductibles. South Florida multifamily property insurance now costs thousands of dollars per door, and negotiations with lenders continually get more involved, noted Chris Conlon, director of risk management at Mahaffey Apartment Company in St. Petersburg, Fla. “Insurance is not a singular factor, but the insurance line item is part of the consideration of where and what to build. Affordable housing is getting killed,” he said.

To be sure, it’s far too soon to confidently predict how weather and expenses will play out in commercial real estate. Temperature forecasts might not turn out as expected. Growth in expenses such as insurance trend could reverse as inflation decelerates. And it will take years to erode the advantage of low-cost areas.

Still, since rapidly rising expenses could limit development and reduce profitability in areas that now carry a pricing advantage, investors should underwrite the risk and not assume it will go away. “The increase in insurance costs in high growth markets such as Florida and Texas is stripping the cashflow out of real estate deals,” said Danielle Lombardo, chair of Lockton Global Real Estate Practice. “If deals don’t pencil as a result of insurance and there is expected continued volatility, real estate owners and developers will look elsewhere.”

The post Will Rising Costs Curb Sunbelt Growth? appeared first on Yardi Matrix Blog.

]]>The post Private CRE Returns Sag in Q4. More to Come? appeared first on Yardi Matrix Blog.

]]>Private real estate values are dropping just as REITs are rebounding from 2022 losses. The difference in performance illustrates the disparity between public and private commercial real estate investment styles, but also begets the question of how much further prices will drop.

Newly released returns reveal private fund values sagged in the fourth quarter of 2022 while REITs staged a fourth-quarter rally in what was still a year of huge price declines. Private real estate funds that comprise major industry indexes fell by roughly 5% in the fourth quarter, their worst performance in decades.

The National Council of Real Estate Investment Fiduciaries’ (NCREIF) ODCE index of core real estate funds fell by 5.0% in the fourth quarter, including a -5.8% appreciation return and 0.8% dividend yield. For the year, the ODCE produced a 7.5% gain, consisting of a 3.9% appreciation return and a 3.5% dividend.

Read also: Banks Positioning for Rising Distress

The Pension Real Estate Association’s (PREA) U.S. AFOE Quarterly Property Fund Index likewise dropped 4.8% in the fourth quarter of 2022, with -5.5% appreciation and 0.5% dividend gains. The net fund return was 7.7% for the full year in 2022, consisting of 5.2% appreciation and 2.5% income gains.

Meanwhile, the NAREIT All-Equity REIT Index returned 4.1% in the fourth quarter but produced total returns of -24.4% during 2022. The REIT index returns during the year included -27.5% appreciation return and a 4.2% dividend yield.

Uncertainty Remains

Commercial property prices hit record highs in the first quarter of 2022, but rising interest and mortgage rates prompted valuations to fall. Investors quickly penalized public REITs, worried about the impact of rising rates and the prospect of an economic downturn that would reduce demand for commercial properties. The equity REIT index returned -17.0% in the second quarter of 2022 and -9.4% in the third quarter before stabilizing. The equity REIT index produced total returns of 5.2% in 4Q 2022 and 9.3% in 1Q 2023.

While REIT shares were dropping starting in the second quarter of 2022, it took several quarters for private fund indexes to record similar price declines. Private real estate funds are appraised only occasionally, so the changes in value are recorded much more slowly. Returns of public and private real estate tend to even out over time, but during periods of market disruption they perform much differently.

The question now for private funds such as those covered by NCREIF and PREA is how much more they will decline before hitting bottom and rebounding. Mortgage rates are now higher than the average early-2022 capitalization rates for most property types. That has prompted a 15% to 25% increase in cap rates, depending on property type, location and property-level income stability.

If cap rates stay at their new level—which is no sure thing, given the unexpected strong performance of the economy—further valuation declines are likely in the offing for private real estate funds, and possibly for some REITs.

The post Private CRE Returns Sag in Q4. More to Come? appeared first on Yardi Matrix Blog.

]]>The post Banks Positioning for Rising Distress appeared first on Yardi Matrix Blog.

]]>Debt availability has diminished, and property owners are being squeezed by an increase in commercial mortgage rates, which have increased by 200-400 basis points since reaching historically low levels in the spring of 2022. The average commercial loan coupon increased to 5.3% in the fourth quarter of 2022, up from 3.3% in 4Q 2021, according to CBRE Research.

The Increased Cost of Capital

The increased cost of capital has put some property owners in a pickle, particularly those that took out adjustable-rate low-coupon loans in 2020-21 that either had interest rate caps expire or are up for refinancing and qualify for less proceeds today.

Speaking at a webinar on the state of the debt markets last week sponsored by the Pension Real Estate Association, Chris Tokarski, co-CEO of ACORE Capital, said that distress has already picked up and “more is coming.” Tokarski noted that in recent years some property owners took out interest rate caps that expired before the loan matured, leading to a huge and unanticipated spike in debt-service payments. The index to which floating-rate loans are tied rose more than 400 basis points since early 2022. Other properties are up for refinancing but qualify for a smaller mortgage because of higher rates, lower property valuations and lenders either exercising caution or being out of the market entirely.

Although the number of distressed loans is starting to increase slightly, the situation will intensify as more loans come up for refinancing and rates stay elevated. An increasing number of borrowers are asking lenders and servicers to extend loans, an echo of the “extend and pretend” regime in the wake of the last downturn in 2008-09.

And though loan extensions are happening, Tokarski and fellow PREA panelist Jeff Friedman, principal of Mesa West Capital, noted there are important differences with the GFC. For one thing, before lenders agree to extend a loan today, they typically require concessions such as paying down the loan balance or adding reserves.

The Change in Interest Rates

There are other differences in circumstances, including the change in rates. In 2008, the commercial real estate market was riding high when the economy crashed, prompting property income and interest rates to drop sharply. Friedman noted that the pre-GFC floating-rate index was 5.25% and fell to .10% to .25% afterwards. In that case, the change in rates worked to the benefit of borrowers, as debt-service payments were lower if a loan was extended at the new, lower market rate.

Today’s distress is also related to liquidity, but mortgage rates have changed from low to higher due to inflation and excess demand in the economy. The Federal Reserve is trying to cool the economy, not jump-start it as was the case in 2008.

Another change from the last downturn is that banks’ balance sheets are healthy, putting them in a better negotiating position. Although commercial lending became more aggressive as the last expansion extended past a decade, leverage did not near the aggressive levels of the 2005-07 period and loan defaults have remained relatively low by historical standards. In 2008, the nation’s banking system was on the verge of crisis owing to defaulted residential and commercial loans exacerbated by trading of credit default swaps.

The extent of the commercial distress today is likely to depend on how long interest rates remain high and the impact on pricing, Tokarski said. “If interest rates settle in at 200 basis points higher, cap rates will settle in (approximately) 200 basis points higher,” he said. With values falling and much uncertainty about pricing, the only sales taking place “need to transact rather than want to transact,” Friedman said.

The circumstance has created an opportunity for high-yield capital to fill the gap between the balance of maturing mortgages and take-out loans. Friedman said that such “rescue” capital is plentiful. He said there are other types of loans that continue to get done, such as stable multifamily and industrial properties and recapitalizations of struggling property types such as office.

The post Banks Positioning for Rising Distress appeared first on Yardi Matrix Blog.

]]>The post CRE Deal Flow Set to Tumble: CREFC appeared first on Yardi Matrix Blog.

]]>The CREFC conference took place as the stock market was plummeting and interest rates were soaring to multi-year highs, which heightened the negative tone. The Federal Reserve raised policy rates this week by 75 basis points, the biggest one-day jump in 28 years, in a bid to cool surging inflation. The consumer price index rose to 8.6% year-over-year in May, led by spiraling housing and energy costs. The 10-year Treasury yield has increased nearly 200 basis points and topped 3.40% this week, its highest level since January 2011.

Although commercial property fundamentals remain healthy in most sectors, the worrisome economic news increases the likelihood of a recession in coming quarters and is likely to put the industry in a holding pattern. “It’s been a while since we last discussed stagflation,” said CREFC executive director Lisa Pendergast. “No doubt, rising rates will impact mortgage and cap rates negatively, and recession can have a deleterious effect on property-level cash flows.”

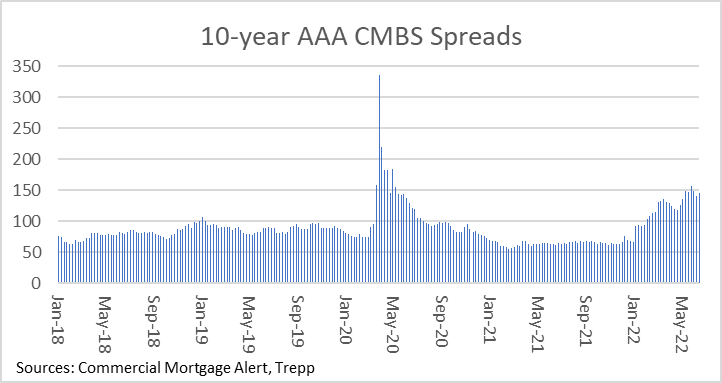

CMBS Spreads Jump

Lenders and borrowers have been hit with a double whammy. Not only are interest rates rising but risk spreads are widening, as well. For example, the spread of senior 10-year triple-A CMBS has increased by more than 80 basis points over the past year, with that class priced to yield 145 basis points over Treasuries in a deal issued this week. The combination of rising rates and higher-risk spreads increased the cost of mortgage debt by 200-250 basis points since the beginning of the year. That creates ripple effects throughout the industry, including:

- Acquisition yields have increased, which erodes pricing. Anecdotally, property values are down 10-15%, but the decline could extend further if the capital markets continue to erode.

- Transaction activity will plummet. “The market is going to slow while people digest what’s going on in the world,” said one CREFC panelist.

- Mortgage activity is dropping. “All-in rates have gone up so much so fast that borrowers are looking at the rate (offered) and saying, ‘No, thank you,’” said a CREFC panelist.

- The increase in rates has the biggest impact on securitization programs, because their origination quotes are directly tied to bond spreads. “Investors don’t want to be in a position where they buy a bond and the next day spreads are wider,” said a CREFC speaker.

- There will also be a deleterious effect on refinancing maturing loans that were originated when rates were lower. Borrowers may be refinancing with less leverage and higher rates, leading to an increase in defaults and/or maturity extensions.

Headed for a Downturn?

The new capital markets environment has even impacted government-sponsored enterprises Fannie Mae and Freddie Mac, which have raised rates and “are not as competitive as other capital sources,” according to multifamily loan executives.

Not every source of mortgage debt will be on the sidelines, though. Portfolio lenders do not have the same mark-to-market constraints and hedging risks of securitized lenders.

Many of the participants at the CREFC event—which hit an all-time-high attendance record of 1,424—forecast that market activity will slow dramatically at least through the end of the summer. Whether the dip extends beyond then will depend on how the economy performs in the second half of the year and the Fed’s ability to slow inflation without creating a sharp recession.

The post CRE Deal Flow Set to Tumble: CREFC appeared first on Yardi Matrix Blog.

]]>The post Self Storage Execs Bullish on Pricing Despite Rising Rates appeared first on Yardi Matrix Blog.

]]>More than $15 billion of self-storage properties traded in 2021, according to Yardi Matrix, more than double any previous year, while prices hit all-time highs. But the recent spike in interest rates is putting the market to the test. The 10-year Treasury rate, which often is used as a proxy for the “risk-free” rate to price transactions, has increased about 150 basis points since January. That has increased fixed mortgage rates commensurately. “In a short time, the cost of capital has spiked dramatically,” noted Tom Hughes, director at Harrison Street Capital.

Panelists at the event in Tarrytown, N.Y., said that the sector is well positioned to thrive in an inflationary environment because income comes from short-term leases and that customer demand is poised to grow because of lifestyle trends.

“There will be some softening of cap rates, but not as large as it should be given the increase in interest rates,” said Brandon Goetzman, a managing principal at the Blue Vista Equity Group. Goetzman was speaking as part of a NYSSA panel moderated by event organizer Nick Malagisi, a managing director at SVN Commercial Real Estate Advisors.

Banks are responding to the rising rates by reducing the amount of leverage they are willing to provide. NYSSA panelists said deals that featured 70% loan-to-value ratios are being lowered to 60% or 65%, with some transactions seeing high bidders drop out as a result. “Some deals are retraded because the winning bidders are not able to perform,” said Devin Huber, a founder of the BSC Group.

How much impact will the increase in financing costs have on acquisition yields? In order to maintain current pricing levels, investors will either have to cut already-thin premiums over the risk-free rate or underwrite continued large growth in rents.

Christian Sonne, an executive vice president at Newmark, said that in self storage the average transaction over the last quarter-century was priced to yield a 3.84% premium over the 10-year Treasury bond. More recently, as storage prices have climbed, investors’ premium has been 1.88%, about half the long-term rate, Sonne said. “I’ve never seen such compressed spreads,” he observed. “Folks are relying on appreciation, not cash flow.”

Yet many in the sector believe that cash flow will keep rising at above-trend levels and prices will remain firm in the face of rising rates. Self-storage rents increased by 10% in 2021, per Matrix, as demand skyrocketed due to demographic and lifestyle trends that were exacerbated by the pandemic.

“The pandemic has created structural growth in self-storage demand,” Sonne said. Investors “believe it is a haven against uncertainty and a hedge against inflation.”

Read the full analysis: NYSSA: Self Storage Prices to Hold Firm as Demand Rises

The post Self Storage Execs Bullish on Pricing Despite Rising Rates appeared first on Yardi Matrix Blog.

]]>The post Returning to the Office: Is That the Future? appeared first on Yardi Matrix Blog.

]]>Few real estate topics generate as much debate. It’s a crucial question within the commercial property industry since there probably are more dollars committed to office buildings than any other property type. Outside the industry, it touches on the daily lives of many.

I’ve noticed a severe disconnect between the views of people within and outside the real estate industry. Property executives stress the benefits of in-person office work; how young people want to return to the office to make connections, collaborate and get mentored; how people are tired of Zoom meetings or working in their pajamas, etc.

Outside the industry, however, I don’t know many people who want to commute regularly and go back to the office unless they absolutely must. Everyone I’ve met whose jobs permanently change to mostly or fully remote are without exception happy.

Few young workers I’ve encountered think of their careers in terms of mentorship and long-term arcs. They’re mostly focused on their immediate work conditions and pay. For most of those raised in the Internet era, working on their laptops at home is a feature, not a bug. And given the shortage of skilled young workers and difficulty companies have preventing valuable employees from being poached, companies have no choice but to accommodate their desires while raising pay and benefits.

Why So Optimistic?

There could be many reasons why the CRE industry may be out of touch with my experience. One possibility is that my experience is not representative. Excluding that, my best guess is a “talking your book” phenomenon. Individuals whose business is selling commercial space naturally want to promote the benefits and necessity of office space.

Another explanation for excess exuberance could be that the pessimistic scenario is disheartening. A sharp drop in demand for offices creates many negative implications for the industry. Much easier to believe that things will work out with minimal disruption.

The nature of our jobs might also play a role. Meeting in person and collaborating with teams is more valuable in finance and real estate than other office-using tasks such as data entry or computer programming. The property industry’s view of the office work experience likely differs from the views of those in other office-using industries.

One thing the CRE industry gets right is that offices are still necessary. The office market is facing a period of painful disruption, but what exactly that entails remains to be seen. Today, onboarding generally involves grafting a few remote newcomers onto a functioning team. Will that be as efficient in five or seven or 10 years, when entire teams are remote and have never been together in person?

Also, much of the leverage for remote work today is on the side of workers, who can demand terms because of the labor shortage. The dynamic changes, though, if the economy slows, unemployment rises, and the leverage turns to the employers’ side. Under that scenario, how many corporations will demand more in-person attendance?

More Questions Than Answers

In the end, my forecast for office space involves a lot more questions than answers. It’s an easy call to say that demand for offices will decline. Many companies have space they aren’t using, and that will prompt cutbacks when leases expire in coming years. That will be offset to some degree by overall growth in office employment and large firms maintaining premier office spaces to attract talent.

Still, demand over time is likely to be negative relative to pre-pandemic levels. Office buildings that aren’t properly amenitized or in bad locations will likely lose tenants and be converted to other uses. Early indications are that rents will level off and office landlords will be forced to reinvent space and spend a lot on tenant improvements.

Beyond that, office work will continue to evolve.

Read the full analysis: The Future of Office: Is CRE Out of Touch?

The post Returning to the Office: Is That the Future? appeared first on Yardi Matrix Blog.

]]>The post Demand for RV/Boat Storage Rising as Sales Hit Record Highs appeared first on Yardi Matrix Blog.

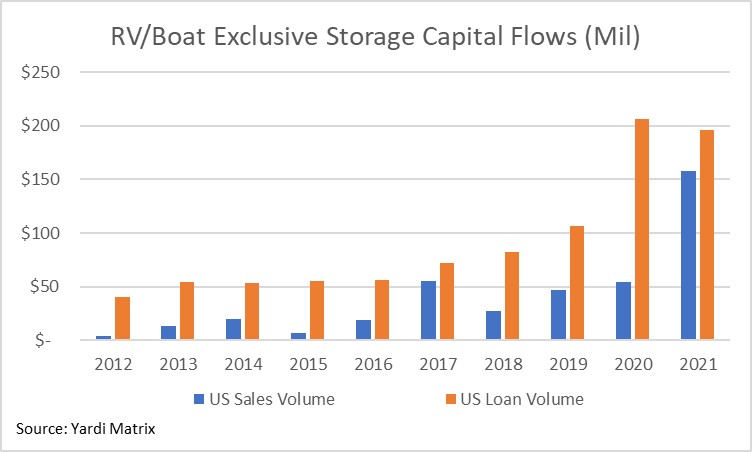

]]>That prompted sales and usage of RVs and boats to hit new highs in 2021. The growth in the segment led Yardi Matrix to create a database of RV/boat exclusive storage facilities as a supplement to its database of self storage properties, which is the largest in the U.S.

Yardi’s database encompasses 786 completed RV/boat exclusive storage properties in the U.S. with 6,850 acres of space and another 35 facilities that are in the development pipeline. Metros with the largest amount of RV/boat storage include Denver, San Francisco, Dallas, Houston and Phoenix. These metros have large populations and are within proximity to parks and campgrounds, RV rental facilities, waterways and large populations.

Yardi’s database finds that Denver leads metros in RV/boat exclusive storage in acreage with 596.8, followed by San Francisco (420.4), Dallas (345.7), Houston (302.9) and Phoenix (299.3). Denver also leads with 47 properties, followed by Houston (45), San Francisco (39), the Inland Empire (36) and Los Angeles (35).

Although it remains relatively small compared to other niche segments of commercial real estate, the industry registered record-high capital flow in 2021, a sign that investors are increasingly taking notice. Some $157.7 million of RV/boat exclusive facilities were sold in 2021, almost triple the previous annual high.

RV/Boat Usage on the Upswing

Data from industry trade groups demonstrates the growth in ownership and usage of RVs and boats. RV wholesale shipments reached a record 600,240 in 2021, up 39.5% over the 430,412 units shipped in 2020 and surpassing the prior record set in 2017 of 504,599 shipments, according to the Recreational Vehicle Industry Association.

Likewise, the acquisition and use of boats is growing. According to the National Marine Manufacturers Association, new powerboat retail unit sales are expected to surpass 300,000 units for the second consecutive year in 2021. Sales in 2021 are expected to be down slightly from 2020, the previous record high, but will be 7% above the five-year average. The NMMA projects 2022 sales to surpass 2021 totals by as much as 3%.

Americans have long had a love affair with RVs and boats, and the RV/boat exclusive storage segment has been around for decades. But like many other developments involving work and migration, the pandemic has created behavioral changes and exacerbated some existing trends.

Foremost among the reasons is the desire to travel and have recreational experiences without crowds. Over the last two years, many Americans avoided airplanes and other forms of public transportation in favor of ground travel.

Another driver of the growth in RV and boat sales is the healthy balance sheets of households as people stopped spending while sheltered in place and collected stimulus checks from the federal government.

Younger Americans also got into the act. The pandemic helped stoke a growing appreciation for recreation and travel to rural settings. What’s more, some found that they could work from remote locations, which means they can live in RVs and work, not just use them for travel.

Yet another development advantageous to RV/boat exclusive storage demand is the growth in Airbnb-type online apps, which enable RV owners to rent vehicles that are parked in storage facilities. The RVIA notes that median annual usage of RVs is 25 days a year, which means that many vehicles are in storage the vast majority of the year. Renting stored vehicles can generate significant income for owners.

Growing Niche

Recreational vehicles and boats are a durable part of the American experience, and economic and social trends indicate that is likely to intensify in coming years. As sales of RVs and boats increase, the demand to store the vehicles is likely to grow. Traditional self storage facilities have limited space and amenities to store RVs and boats, which means that demand for RV/boat exclusive facilities will likely grow as RV and boat sales rise.

Growth of RV/boat exclusive facilities might be constrained by the cost of land, the amount of acreage needed to house vehicles and the fact that the facilities are geared toward specific objects as opposed to general usage. At the same time, though, the growing demand from RV and boat sales combined with the limited amount of supply means the segment’s fundamentals should remain healthy, even in volatile economic times.

Read the full Matrix Bulletin-RVBoat Storage-March 2022

The post Demand for RV/Boat Storage Rising as Sales Hit Record Highs appeared first on Yardi Matrix Blog.

]]>The post Loan Quality Stable as Volume Rises appeared first on Yardi Matrix Blog.

]]>Commercial property values and loan origination volumes are reaching all-time peaks as investors flock to the sector. The Mortgage Bankers Association forecasts that commercial and multifamily borrowing will break $1 trillion for the first time in 2022, up 13% from estimated 2021 volume of $900 billion.

Meanwhile, CBRE’s lending index of debt market conditions rose 10.3% in the fourth quarter and is 42% above pre-pandemic levels, a sign that lending activity and liquidity are strong and credit spreads are tight. At the same time, CBRE reported that metrics that gauge loan quality such as the average loan-to-value (LTV) and debt-service coverage ratio (DSCR) were roughly the same as they were in 2018.

CBRE found that the average LTV of loans originated in 4Q21 was 63.4%, down slightly from 64.0% in 4Q20 and 65.3% in 4Q18. The average DSCR was 1.48 in 4Q21, which means that net property income was almost 50% more than the average loan payment. The 4Q21 DSCR was up slightly from 1.47 in 4Q20 and 1.42 in 4Q18.

Loan quality is boosted in part because of market conditions such as low interest rates and thinning yields, or capitalization rates, that investors are willing to accept to own properties. The average cap rate in CBRE’s loan universe was 5.1% in 4Q21, down 4 basis points from the year-earlier period and 77 basis points below cap rates in 4Q18. Lower cap rates increase property values and reduce borrower LTVs.

Meanwhile, low interest rates in recent years and tighter credit spreads have contributed to historically low loan coupons, which means borrowers can take out more debt with lower monthly payments than they could in the past. The average coupon in CBRE’s loan universe dropped to 3.3% in 4Q21, unchanged from 4Q20 but well below the 4.7% average in 4Q18.

Just over one-quarter (26%) of loans originated in 4Q21 had coupons of less than 3.0%, and 70% had coupons between 3.0% and 4.0%. Larger loans—usually with better-capitalized borrowers—were more likely to have lower rates.

CBRE’s index highlighted the increasing market share of alternate lenders—including debt funds, pension funds and credit companies—which originated 37% of non-agency loans in the fourth quarter of 2021, more than any other category of lender. Banks had a 29.0% market share, followed by CMBS (18.5%) and life companies (14.8%).

Surviving Rising Rates

Heady capital conditions reflect the commercial property market’s strong fundamentals performance, high returns relative to fixed-income products, and reputation as an inflation hedge. Rents in some property sectors—such as multifamily, industrial and self-storage—rose in 2021 at decades-long highs. Meanwhile, commercial real estate has traditionally produced competitive returns during periods of high inflation at a time when rising prices are a main economic concern.

“Commercial real estate lending volumes are closely tied to the values of the underlying properties. In 2021 those values rose by more than 20%, and those increases will fuel further demand for mortgage debt in the coming years,” said Jamie Woodwell, MBA’s vice president for commercial real estate research.

There are looming issues, though, that should concern the market. The Federal Reserve is expected to increase policy rates between 100 and 200 basis points over the next 12 to 18 months, which likely will push the 10-year Treasury rate up significantly. The 10-year-Treasury yield topped 2% last week for the first time since July 2019 and is expected to keep rising.

Since loans and properties are priced off the Treasury risk-free rate, cap rates could rise over the next 12 to 24 months. Although there is not a one-to-one correlation between Treasury yields and cap rates, a sharp increase in interest rates would put pressure on property prices and increase the cost of borrowing. Rising loan coupons will especially hurt when today’s low-coupon loans mature and must be refinanced.

Moody’s Analytics Chief Economist Mark Zandi said last week during a webinar sponsored by the Counselors of Real Estate trade group that commercial real estate prices would flatten as interest rates rise, while some property segments such as gateway offices face “game-changer” complications such as work-from-home that could reduce occupier demand. “Commercial real estate is a good hedge, but there is no way to get away from the reality of work-from-home and higher cap rates,” he said.

The good news is that loans underwritten in the current cycle are much better prepared to handle stressed market conditions than was the case before the global financial crisis. One loan analyst noted that when loans originated in the 2005-07 period were analyzed using stressed scenarios (such as higher interest rates and an economic recession), more than a quarter had stressed LTVs of more than 100%, and nearly half had stressed LTVs of at least 90%. Using the same stressed standards, much fewer loans originated in recent years fail the tests.

“What matters in all this is a loan’s ability to refinance under stressed scenarios,” the analyst said. “There is more risk in a rising rate environment, more debt per square foot is a concern, but (conditions) haven’t deteriorated to pre-financial crisis levels.”

Said Woodwell: “Continued increases in property incomes, and stability in the ways investors value those incomes, should also support solid demand for mortgage capital, even in the face of modest increases in interest rates.”

The post Loan Quality Stable as Volume Rises appeared first on Yardi Matrix Blog.

]]>The post Construction Employment Recovering, but Still Short Workers appeared first on Yardi Matrix Blog.

]]>Construction employment rose in 231, or 65%, of 358 metro areas in 2021. The Houston metro added the most construction jobs (8,800 jobs, up 4%), followed by Chicago (6,500 jobs, up 5%) and Los Angeles (6,300 jobs, up 4%).

Sioux Falls, S.D., had the highest percentage gain (24%, 2,100 jobs). Among larger metros, the biggest percentage gains were achieved in the Midwest: St. Louis (9%, 5,700 jobs) and Milwaukee (9% 2,500 jobs) topped the list, while Cincinnati, Cleveland and Pittsburgh were all up 8%. Construction employment declined from a year earlier in 76 metros and was flat in 51.

Long Island, N.Y., lost the most jobs (-5,700, or -7%), followed by New York City (-4,200 jobs, or -3%) and Baltimore (-3,800 jobs, or -5%). The largest percentage declines were in Evansville, Ind.-Kentucky (-18%, or -1,700 jobs) and Napa, Calif. (-15%, or -600 jobs). Seven areas set all-time lows for December, while 57 metros reached new December highs for construction jobs.

Twenty-six states remain below the pre-pandemic construction employment levels of February 2020, with losers led by New York (-42,000 jobs, or -10%), Texas (-30,200, -3.9%) and California (-22,300, -2.4%), according to the AGC. Louisiana had the largest percentage loss (-13%, -17,200 jobs), followed by Wyoming (-11%, -2,500) and New York.

New York and California have been affected by pandemic restrictions, and California and Texas have lost some jobs due to weather events over the last 22 months. Construction activity in Texas and Louisiana has also been hit hard by the steep downturn in oil and gas activity, onshore and offshore, said Ken Simonson, the AGC’s chief economist.

Since the pandemic started, Utah has added the most jobs (10,000, 8.8%), followed by Washington (8,200, 3.7%) and North Carolina (7,900, 3.4%). South Dakota added the highest percentage (10%, 2,500 jobs), followed by Utah and Idaho (8.2%, 4,500). In February, construction employment reached a record high in Massachusetts, Utah, Washington and the District of Columbia.

Labor Shortage

Job openings in construction totaled 273,000 at the end of December, an increase of 62,000, or nearly 30%, from December 2020, according to the government’s latest Job Openings and Labor Turnover Survey. That figure exceeded the 220,000 employees that construction firms were able to hire in December, implying firms would have added more than twice as many workers if they had been able to fill all openings, Simonson said.

“Construction employment topped year-earlier levels in almost two-thirds of metros for the past few months,” he said. “But contractors in many areas say they would have hired even more workers if qualified candidates were available.”

The growing number of construction job openings is a clear sign that labor shortages are getting worse. AGC executives noted that the association’s recently released 2022 Construction Hiring and Business Outlook found that 83% of contractors report having a hard time finding qualified workers to hire. They urged Congress and the Biden administration to boost funding for career and technical education to help recruit and prepare more people for high-paying construction careers.

“For every dollar the federal government currently invests in career and technical education, it spends six urging students to attend college and work in an office,” said Stephen Sandherr, the association’s chief executive officer. “Narrowing that funding gap will help more people understand that there are multiple paths to success.”

The post Construction Employment Recovering, but Still Short Workers appeared first on Yardi Matrix Blog.

]]>The post What’s in Store for Multifamily in 2022 appeared first on Yardi Matrix Blog.

]]>Panelists at the National Multifamily Housing Council’s Annual Meeting in Orlando last week predicted a deceleration in the heady growth rates achieved in 2021 for the economy and the multifamily segment. Nonetheless, experts expect the strong fundamentals performance will continue, driven by robust economic growth, healthy consumer balance sheets, pent-up demand from the pandemic and the long-term shortage of housing.

Multifamily is coming off a year with the highest asking rent increases ever, due to extremely strong demand that lifted occupancy rates near all-time highs. Although growth is expected to moderate in 2022, the industry does face challenges that include rising interest rates, a national labor shortage, evolving migration patterns, and changes in renter preferences.

Economic Growth with Headwinds

Richard Barkham, global chief economist & global head of research for CBRE, said he expects GDP to increase by 4% to 4.5% in 2022, driven by robust spending by consumers and businesses. However, he said inflation will remain high before settling down into the 2.5% to 3% range. The fear of an inflationary spiral is prompting the Federal Reserve to increase policy rates and sell off some of its bond holdings.

Barkham said the increase in interest rates “is a sign of success, a sign of recovery in the economy.” However, he said there are headwinds that include inflation, rising rates, the labor shortage that has driven wage growth, and a potential economic slowdown in China and emerging markets.

Barkham said that the decline in immigration in recent years means that the U.S. will have 2 million fewer workers than was projected in the past. “If trends continue, the U.S. labor force will shrink for the first time in generations,” he said, noting that the drop would put a crimp in future economic growth. The tight labor market has produced 20-year-high wage growth, with the average wage rising about 5% in 2021.

Sustained Rent Growth

Rising wages have played a role in the apartment market, providing households with the ability to pay for the 13.5% increase in U.S. apartment asking rents in 2021, according to Yardi Matrix data. A big part of rising rents is the rent growth in luxury apartments. Rents for luxury Lifestyle units in the U.S. rose by 15.9% in 2021, compared to 11.0% growth for Renter-by-Necessity units, per Matrix. Renters have more to spend on housing for many reasons, including government stimulus, higher wages, and increased savings during the pandemic.

Another factor in rent growth is the migration of renters to secondary and tertiary markets that was exacerbated during the pandemic. Renters that moved to less expensive markets were able to pay more for rent because it was relatively cheap compared to the higher-rent markets they moved from. Because of the wave of population growth, asking rents in 2021 rose by 20% or more in many markets in the Sun Belt and Southwest, despite large increases in apartment deliveries in those metros.

Migration is closely related to trends in work-from-home. Return to offices has been delayed as new variants of COVID-19 continue to emerge, disrupting corporate plans and making it difficult to develop permanent policies. Yardi Matrix vice president Jeff Adler said it will take another couple of years before workplace issues shake out.

Adler said the pandemic exacerbated existing migration trends. He said population will continue to shift from urban to suburban submarkets within the same metro and from high-cost gateway markets to secondary and tertiary markets with a lower cost of living and appealing lifestyle amenities. As people continue to seek urban-style amenities such as restaurants and entertainment, secondary metros and outer-ring suburbs are developing “urbanized nodes” that appeal to renters, he said.

Speaking on a different panel, John Affleck, senior vice president at John Burns Real Estate Consulting, agreed. “What we’re seeing today is a strategic location change from people who realize they are not going back to the office anytime soon,” he said.

The growth outside of gateway markets is having a huge impact on investment strategies. Ned Striker, senior managing partner of investments and capital markets at Cortland, said that over the last decade institutional investors have become more comfortable with secondary and tertiary markets that they would have avoided in the past because they were too small and illiquid.

Read the full analysis: Multifamily Demand Remains Strong

The post What’s in Store for Multifamily in 2022 appeared first on Yardi Matrix Blog.

]]>